Compound interest is one of the most important concepts in finance. It determines how investments, savings accounts, and loans grow over time when interest is added back to the balance at regular intervals. Daily compounding, in particular, is common in savings accounts and short-term investments. With Excel, you can create a powerful daily compound interest calculator that updates automatically based on your inputs.

Compound interest is one of the most important concepts in finance. It determines how investments, savings accounts, and loans grow over time when interest is added back to the balance at regular intervals. Daily compounding, in particular, is common in savings accounts and short-term investments. With Excel, you can create a powerful daily compound interest calculator that updates automatically based on your inputs.

Key Takeaways

- Compound interest grows your balance by adding interest back into the principal daily.

- Excel formulas make it easy to calculate daily compound interest for any period.

- The formula structure is

=Principal*(1+Rate/365)^(365*Years). - You can expand the calculator with helper columns, conditional formatting, or VBA automation.

- A downloadable workbook is included so you can practice immediately.

Table of Contents

Understanding Daily Compound Interest

Compound interest works by applying interest to the principal plus any previously earned interest. The frequency of compounding determines how often this happens. With daily compounding, interest is applied 365 times per year. The general formula is:

Future Value = Principal * (1 + Rate/365)^(365*Years)Where:

- Principal = Starting balance

- Rate = Annual interest rate

- Years = Number of years invested

- 365 = Number of compounding periods per year

Step-by-Step: Building a Daily Compound Interest Calculator in Excel

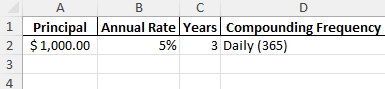

Step 1: Set Up Input Data

In your Excel worksheet, create input fields:

Principal: 1000

Annual Rate: 5%

Years: 3

Compounding: Daily (365)

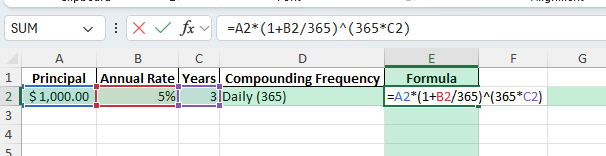

Step 2: Enter the Formula

In a new cell, type:

=A2*(1+B2/365)^(365*C2)This multiplies the principal by the daily compounding growth over the chosen number of years.

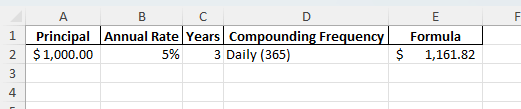

Step 3: Format the Result

Format the result cell as Currency or Number for easier readability.

Step 4: Test with Sample Data

Using the sample data (Principal = 1000, Rate = 5%, Years = 3, Daily compounding), the result should be approximately 1161.82.

Common Mistakes and How to Fix Them

Forgetting to divide by 365: Always adjust the rate for daily compounding by dividing by the number of periods per year.

Mixing percentage and decimal: Ensure the annual rate is formatted as a decimal (5% = 0.05) when applying formulas.

Incorrect exponent: The exponent must be total compounding periods (365 * Years).

Using text inputs: Make sure inputs like principal and rate are numbers, not text, or the formula will fail.

Bonus Tips and Advanced Scenarios

Create a Year-by-Year Breakdown: Use a table with helper columns for each year and calculate balance progression with formulas like =PreviousBalance*(1+Rate/365)^365.

Power Query Automation: Load investment data from an external file and calculate compound interest automatically when refreshing the query.

VBA User Form: Create a simple form with input boxes for principal, rate, and years. VBA can calculate and display the result dynamically:

Sub DailyCompoundInterest()

Dim P As Double, R As Double, Y As Double, FV As Double

P = Range("A2").Value

R = Range("B2").Value

Y = Range("C2").Value

FV = P * (1 + R / 365) ^ (365 * Y)

MsgBox "Future Value after " & Y & " years: " & Format(FV, "Currency")

End Sub

Use Cases for Daily Compound Interest Calculations

Daily compound interest calculations are practical in many scenarios, from personal finance to business planning. Below are detailed examples showing how different groups can apply this concept in Excel for better financial decision-making.

1) Personal Savings Growth

Context: Many savings accounts and money market accounts use daily compounding. Knowing how to project balances helps individuals understand the benefits of keeping funds invested longer.

How to use in Excel:

Create input cells for principal, annual rate, and number of years.

Apply the formula =Principal*(1+Rate/365)^(365*Years) to calculate the future balance.

Set up a table to compare different rates or durations side by side, showing how balances change with time.

Benefits:

Helps savers visualize how small deposits can grow significantly over time with compounding.

Encourages long-term saving habits by showing clear, numeric outcomes.

Supports better decisions on where to keep emergency funds or longer-term reserves.

2) Investment Planning and Forecasting

Context: Investors often evaluate returns from stocks, bonds, or certificates of deposit (CDs) that may use daily compounding for interest accrual. Accurate forecasting ensures informed choices between alternatives.

How to use in Excel:

List possible investments with different rates of return and compounding frequencies.

Use formulas like =Principal*(1+Rate/Compounding)^(Compounding*Years) to calculate future values for each.

Create scenario tables or use Data Tables (What-If Analysis) to model multiple outcomes at once.

Benefits:

Provides side-by-side comparisons of investment options with clear financial projections.

Helps investors identify the effect of compounding frequency on returns.

Supports financial advisors in presenting clients with transparent, data-driven recommendations.

3) Loan Cost Analysis

Context: Some loans and credit products apply interest on a daily basis. Borrowers need to know the real cost over time, including how daily compounding increases total repayment amounts.

How to use in Excel:

Enter loan amount, interest rate, and loan duration into input cells.

Use the daily compounding formula to calculate the total amount owed at the end of the loan term.

Extend the model by including scheduled payments with helper columns that reduce principal and reapply compounding each day.

Benefits:

Provides borrowers with a realistic picture of loan obligations, beyond simple annual rate advertising.

Reveals how frequent compounding affects costs, allowing smarter borrowing decisions.

Assists in comparing different repayment schedules to minimize total interest paid.

4) Educational Exercises and Training

Context: Teachers, students, and trainers can use compound interest examples to illustrate exponential growth and financial literacy concepts. Daily compounding is a practical example of how mathematics applies to real-world finance.

How to use in Excel:

Ask students to build calculators with principal, rate, and years as inputs, then apply formulas step by step.

Introduce helper columns to show balances year by year using =(PreviousBalance*(1+Rate/365)^365).

Use charts to visually display growth over time with different compounding frequencies (daily vs monthly vs yearly).

Benefits:

Demonstrates the power of compounding through clear, interactive examples.

Teaches Excel skills alongside financial concepts, reinforcing applied learning.

Prepares students to use spreadsheets for real financial planning in their personal and professional lives.

5) Business Forecasting and Financial Management

Context: Companies often hold cash reserves, short-term investments, or interest-bearing accounts. Forecasting balances with daily compounding allows for better cash flow planning and more accurate budgeting.

How to use in Excel:

Set up a model with input fields for corporate reserves, interest rates, and time horizons.

Apply daily compounding formulas to calculate projected balances under different scenarios.

Combine with dashboards that show how reserve balances will look at quarter-end, year-end, or over multi-year horizons.

Benefits:

Improves accuracy of financial forecasts and planning decisions.

Helps businesses maximize the return on idle cash by selecting accounts with favorable compounding terms.

Supports investor reporting by providing transparent growth projections of company reserves.

FAQ

What does daily compounding mean?

It means interest is added back into the balance every day, so each new day’s interest is calculated on a slightly larger balance.

How do I adjust the formula for monthly or quarterly compounding?

Replace 365 with 12 for monthly, or 4 for quarterly, in the denominator and exponent.

Does Excel handle leap years when using 365?

Excel assumes 365 days unless you manually adjust for leap years. Use 366 if needed for exact calculations.

Can I calculate compound interest with irregular contributions?

Yes, add contributions into the balance each period, then apply the formula iteratively or with a helper table.

What if my interest rate is given as a percentage?

Convert it to decimal form in the formula (e.g., 5% = 0.05).

John Michaloudis is a former accountant and finance analyst at General Electric, a Microsoft MVP since 2020, an Amazon #1 bestselling author of 4 Microsoft Excel books and teacher of Microsoft Excel & Office over at his flagship MyExcelOnline Academy Online Course.